Network Performance Optimization

Network Performance Optimization

Industries

Industries

Improved delivery, better visibility: How Accedian and VMware are working together to help CSPs navigate the 5G world

Improved delivery, better visibility: How Accedian and VMware are working together to help CSPs navigate the 5G world

Adding a new dimension of visibility to the Cisco Full-Stack Observability portfolio with Accedian Skylight

Adding a new dimension of visibility to the Cisco Full-Stack Observability portfolio with Accedian Skylight

Tools & Support

Tools & Support

Case Study

See How Groupe BPCE Uses Skylight to Drastically Reduce Their Resolution Time

Read their story

Accedian is now part of Cisco |

Cloud Visibility

Cloud Visibility

Application Performance

Application Performance

Platform

Platform

About Us

About Us

Learn

Learn

Blogs

Blogs

Get your copy of “Optimizing Network & Application Performance For Financial Services Organizations”

Get your copy of the Solution Brief

For banking, financial services, and insurance companies around the world, being technologically-focused, agile, and seamlessly connected with customers and partners is not just a strategic mission, but a critical imperative. This sector is undergoing significant transformation at an accelerated rate of technological change driven by the:

The technological disruption taking place means that speed and accuracy in collecting and analyzing data from a broad range of devices, multi-cloud environments, and disparate systems can mean all the difference between significant profit and catastrophic loss.

of banking and payment companies will be at risk from technological disruption by 2020, while one in five insurance, wealth management, and asset management firms will be at risk

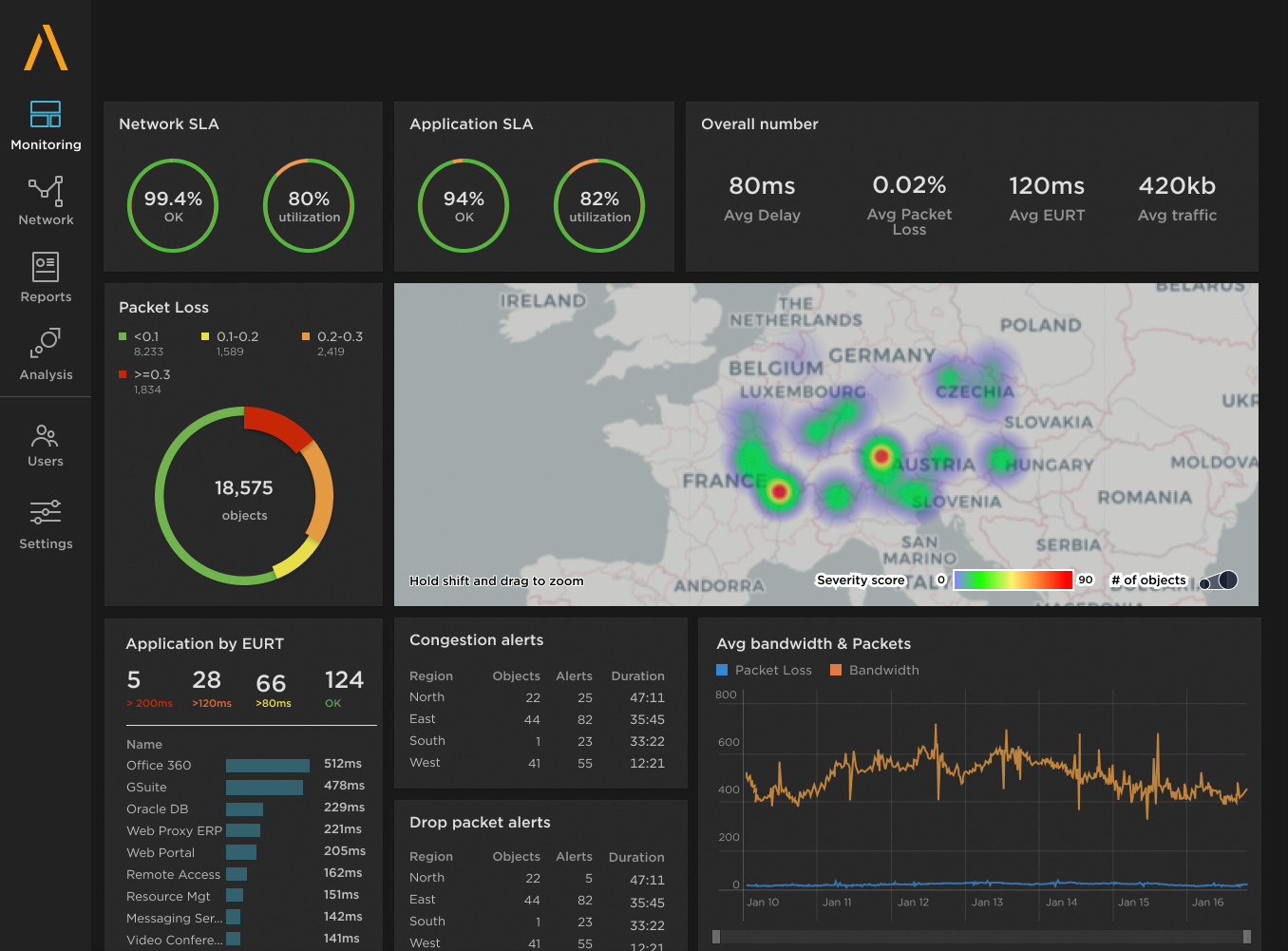

Skylight’s single pane of glass gives you full control of end user experience

Skylight’s compact, structured metadata saves on storage and provides high definition visibility into every transaction

Speed up problem solving and quickly identify what’s causing service degradation with the fastest resolution times (MTTR)

Skylight detects the invisible microbursts that are slowing down your network with exceptional granularity

Moving applications to the cloud and deploying agile, high-performance networks are a key part of digital transformation for the financial services industry. Financial institutions need to be focused on cutting-edge technology and agile in adopting new solutions in order to stay ahead of the competition and deliver flawless experiences for customers and partners.

Performance degradation is unacceptable and even minor packet-loss, minimal delay and almost imperceptible microbursts can impact customers and end users significantly.

Skylight can instrument all of the enterprise WAN circuits, including SD-WAN, and build in activation testing, microburst metering, remote packet capture, and more at a low TCO. Skylight offers an efficient metadata approach for Layer 2 to 7 active and passive monitoring which can save you 300-900% on storage and bandwidth costs.

Skylight actively monitors application performance end-to-end across your network, from HQ to remote branches. It detects microbursts, delay, and packet loss that impacts your end user productivity and customer experience.

Skylight also monitors actual network traffic, application transaction times, and client server delays. The complete view of network and application performance across the full stack lets you pinpoint issues that are impacting your end users.

Many banks still rely on dated and disjointed tools and processes for monitoring, testing and maintaining business-critical networks and applications. Skylight analytics together with telemetry and machine learning correlate performance data in near real time to quickly pinpoint and troubleshoot issues and use predictive analytics to prevent faults.